Proposals to eliminate the tax exemption on municipal bonds are not new and have arisen in every debate over tax reform. On each such occasion, the industry has not emerged wholly unscathed. For instance, in 2017, the tax exemption on advanced refunding was eliminated. The good news is that the market innovated new work-around structures. We would expect that, more likely than not, one or more sectors/bond types will be impacted at the conclusion of this process.

Whatever the outcome, we would not expect the reconciliation process to be concluded until later this year. Finally, we believe that the tax-exempt share (93%) of the ~$4.1 trillion in outstanding municipal bonds, is likely to be grandfathered through maturity, with any repeal of the tax-exemption affecting future issuance.

Heading into the first quarter, One Oak Capital Management’s end of 2024 newsletter advised investors to recognize that after two years of spectacular performance, there were significant risks in large allocations to the equity markets and that reallocating funds into fixed income should be actively considered.

The year began on an optimistic note as the new administration’s pro-business and deregulation policies were lauded and expected to translate into a stronger economy and stronger markets. A continuation of the previous year’s economic robustness coupled with innovations like AI enhancement successfully generated broad optimism. However, the quarter was tarnished with relentless talk of tariffs which inevitably generated mounting concerns regarding economic sustainability and lingering inflation. This created a possible stagflationary environment, which drove risk tolerance lower.

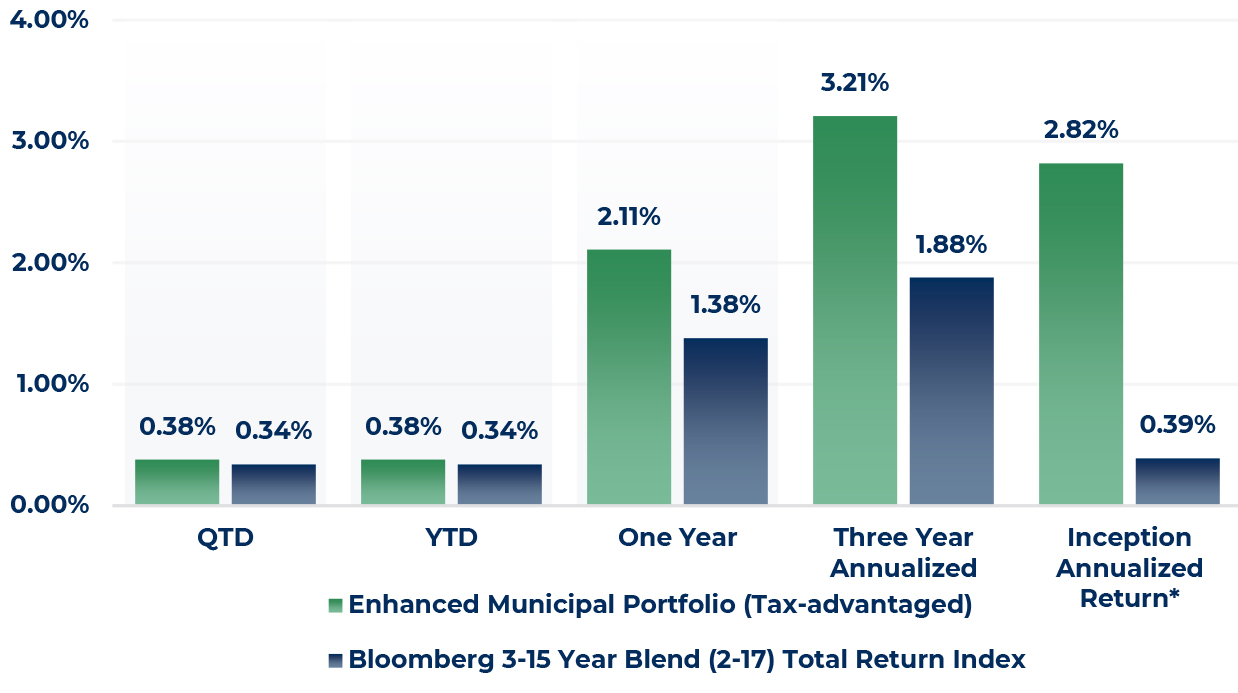

The municipal bond market entered 2025 with a backdrop of strong credit fundamentals, elevated yields, and expectations of robust issuance, as noted by various analysts late in 2024 and early 2025. Yields started the year at notably high levels, driven by a combination of heavy supply in 2024 and shifting Federal Reserve policy expectations. From a technical perspective, demand held firm early in the quarter, with inflows into municipal bond funds and ETFs continuing a recovery from the significant outflows of 2022-2023.

By March, policy uncertainty, particularly around tax reforms and the potential extension of the Tax Cuts and Jobs Act, loomed large. While a full repeal of the tax-exempt status was deemed unlikely (as noted above), given its limited revenue impact relative to the $5 trillion cost of extending the TCJA, speculation contributed to late-quarter volatility. This, coupled with negative seasonality, caused March 2025 to be the worst month for municipal spreads compared to US Treasuries since March of 2020.

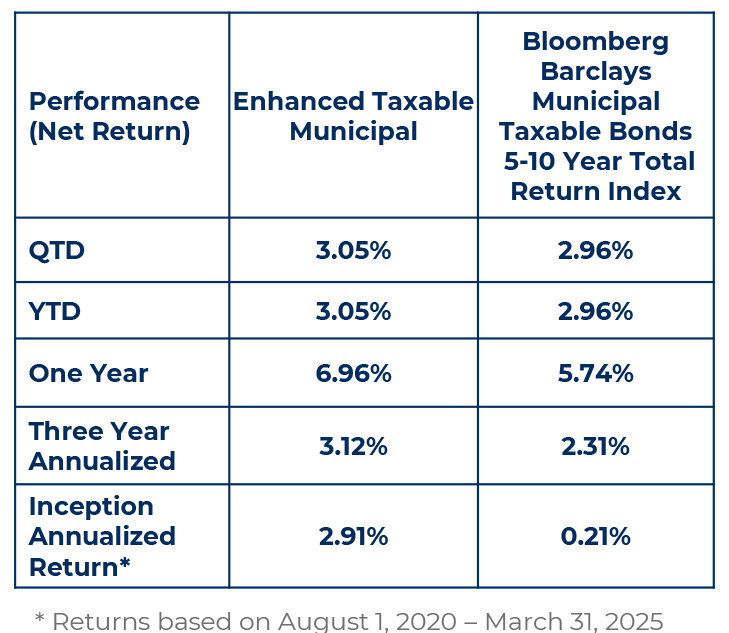

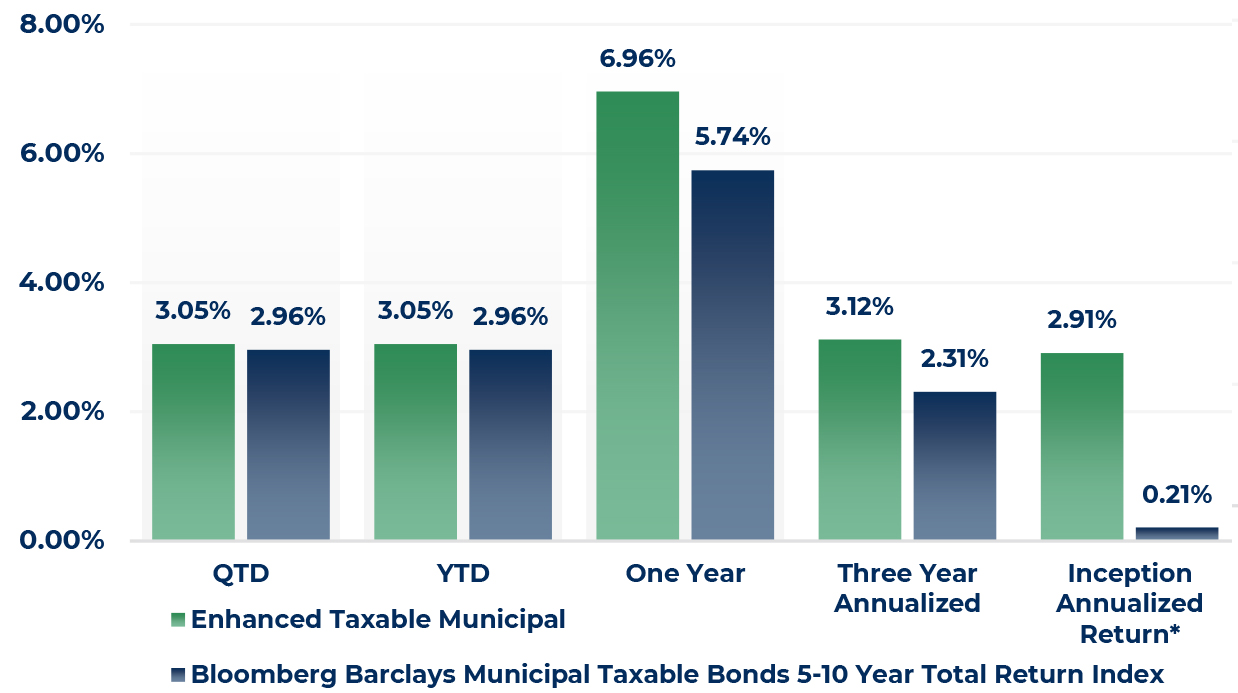

First Quarter 2025 Taxable Municipal Market Review

In January taxable fixed income yields were attractive, with many at their highest levels in years. However, taxable municipal market spreads to corporates tightened in January, with both 30yr AA and A-rated taxable municipals rich to the US Corporate market. Taxable municipal market spreads to corporates continued to tighten in February and a portion of March before widening out somewhat later in the month with both 30yr AA and A- rated securities rich to the US corporate market. Taxable municipals look attractive for most countries on a cross-currency equivalent basis.

For the remainder of 2025, municipal bonds are expected to offer a compelling opportunity for investors, particularly those in higher tax brackets, driven by attractive yields and solid credit fundamentals. Income is likely to remain the primary driver of returns.

The market has experienced volatility which has caused yields to increase and ratios to widen. The increased volatility and credit spread widening the market is experiencing is good news for One Oak’s investment vehicles as it means a significant expansion of their opportunity set.

The team would like to thank you for being a valued investor. Thank you for staying the course with us and we will work hard to deliver solid performance for the remainder of 2025.

Until next time,

One Oak Capital Management is an SEC-registered investment adviser and manager of separately managed portfolios. Registration as an investment adviser does not imply a level of skill or training. This presentation is not an offer to sell, or the solicitation of an offer to purchase, any investment managed or sponsored by One Oak Capital Management or any of its affiliated entities (collectively, “One Oak”). The index shown is provided for illustrative purposes only, is unmanaged, reflects the reinvestment of income and dividends, and does not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indices have limitations because indices have volatility and other material characteristics that may differ from a particular OneOak strategy. One Oak's performance may differ substantially from the performance of an index. In addition, data used in the benchmark are obtained from sources considered to be reliable, but One Oak makes no representations or guarantees with regard to the accuracy of such data. The EnhancedMunicipal Portfolio uses active management and is not benchmarked to the index.

Past performance is not representative of future return performance. Net returns are calculated by deducting the highest standard fee from the gross returns on a quarterly basis. The returns reflect the net performance of employing One Oak's highest fee, 0.30% per year to the gross performance. Net returns do not include any additional intermediary fees that may be charged to the end investor. The presentation and the net performance is meant for financial professionals use only and is not intended for distribution to the end users. The returns include the reinvestment of dividends, interest, and other earnings. The information provided was calculated by One Oak Capital Management, LLC using a combination of proprietary and external data sources and has not been audited for accuracy. While interest on municipal bonds is generally exempt from federal income tax, it may be subject to the federal alternative minimum tax, or state or local taxes. Profits and losses on federally tax-exempt bonds may be subject to capital gains tax treatment. Fixed income risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. One Oak's management fees are deducted each quarter on the first month of the quarter: January, April, July and October. One Oak does not accrue its management fee for the remaining months and therefore the net performances for those months will be higher and does not represent the actual annual net returns.

Due to various risks and uncertainties, actual events, results or the actual performance of the investment may differ materially from those reflected or contemplated in the returns presented within. While assumptions underlying various statements as to the future performance are believed to be reasonable in nature, prospective investors should make their own assessments as to such assumptions and the associated risks, including the likelihood of the strategy achieving the corresponding results. All of which are subject to risks and uncertainties many of which are beyond the control of the investment adviser. As such, no assurance is given as to the realization of any such future performance. No representation or warranty is made as to the future performance or such forward-looking statements. The delivery of this presentation does not imply that any other information contained herein is correct as of any time subsequent to the presentation date. Actual performance results may differ from composite returns, depending on the size of the account, investment guidelines and /or restrictions, inception date, and other factors. One Oak Capital Management, LLC ("One Oak") claims compliance. with the Global Investment Performance Standards (GIPS) and has prepared and presented this report in compliance with the GIPS standards. One Oak has been independently verified for the periods 2019 through 2022.

Fees and yields are calculated by One Oak as of 07/22/25. Prospective investors are encouraged to consult a tax professional before making the decision to invest. Source: Schwab Data as of July 22, 2025. For illustrative purposes only. The framework discussed herein is hypothetical and does not represent the investment performance or the actual accounts of any investors or any funds. The results achieved in our simulations do not guarantee future investment results. It is possible that the actual results of an investor who invests in the manner these projections suggest will be better or worse than the projections, and that an investor may lose money by investing in the manner the projections suggest. The index is included for illustrative purposes only, is not available for direct investment and does not reflect the deduction of fees or expenses which would reduce returns.Actual performance results may differ from composite returns, depending on the size of the account, investment guidelines and /or restrictions, inception date, and other factorsTo invest with One Oak Capital Management LLC, you must be a qualified or accredited investor. Different share classes may have different results. Consult your individual statement.

These materials contained confidential and proprietary information and have been provided with the express understanding that their distribution or the divulgence of any of their contents to any person, other than the person(s) to whom they were originally delivered and such person’s advisors, without the prior consent of One Oak is prohibited.

To invest with One Oak Capital Management LLC, you must be a qualified or accredited investor. Different share classes may have different results. Consult your individual statement.

For more information regarding the Morningstar Rating methodology please visit www.morningstar.com/content/dam/marketing/shared/research/methodology/771945_Morningstar_Rating_for_Funds_Methodology.pdf

The PSN Municipal Universe consists of 213 strategies, across 98 firms. PSN utilizes a proprietary of our clients’ top priority performance screens. PSN Top Guns runs products in six proprietary categories in over 50 universes. This is a highly anticipated ranking and is widely used by institutional asset managers

References made to awards/rankings are not an endorsement by any third party to invest with One Oak and are not indicative of future performance. Investors should not rely on awards/rankings for any purpose and should conduct their own review prior to investing

One Oak Capital Management has done several tax-harvesting trades for the Enhanced and Enhanced Taxable Municipal Portfolio

Logos are protected trademarks of their respective owners and One Oak disclaims any association with them and any rights associated with such trademarks.